John Hancock Life Insurance Review (Coverage Comparisons & More)

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Licensed Insurance Agent

Travis Thompson has been a licensed insurance agent for nearly five years. After obtaining his life and health insurance licenses, he began working for Symmetry Financial Group as a State Licensed Field Underwriter. In this position, he learned the coverage options and limits surrounding mortgage protection. He advised clients on the coverage needed to protect them in the event of a death, critica...

Travis Thompson

Senior Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Senior Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Updated January 2020

Life: Summary-Overview-of-John-Hancock

| Key Info | Company Specifics |

|---|---|

| Year Founded | 1862 |

| Current Executives | CEO (John Hancock) - Marianne Harrison CEO (John Hancock Insurance) - Brooks Tingle |

| Number of Employees | 7,959 |

| Total Assets | $549,407,600,000 |

| Headquarters Address | 200 Berkeley Street, Boston, MA 02116 |

| Phone Number | 1-800-387-2747 |

| Company Website | www.johnhancockinsurance.com |

| Premiums Written - Individual Life | $4,651,894,000 |

| Premiums Written - Group Life | $5,541,041 |

| Financial Standing | -33.1% from Previous Year |

| Best For | Interactive Policies |

Shopping for life insurance can be an intimidating process. With the financial security of your loved ones at stake, there is a lot of pressure to choose the right policy from the right company.

But with so many options on the market, it can be challenging to narrow down the best choices for your particular financial need.

John Hancock is one of the largest life insurers in the country, backed by an even larger global company. They have been providing families with the promise of financial security since 1852.

They are also at the forefront of offering technology-driven, interactive policies that reward policyholders for healthy behaviors.

This extensive review is designed to give you a complete overview of the company and preview all of its policy options to help you decide if John Hancock is the life insurer for you.

Start comparing life insurance rates now by using our FREE tool above!

Table of Contents

John Hancock’s Ratings

The following third-party ratings give insight into John Hancock’s financial strength, business practices, and quality of customer service.

A.M. Best

A.M. Best ratings measure an insurer’s financial strength and its ability to pay all of its policy obligations. John Hancock has an A+ rating, the second-highest possible, meaning they have an excellent ability to meet their financial commitments.

Better Business Bureau (BBB)

The Better Business Bureau assigns one of 13 letter grades based on factors such as time in business, open complaints, resolved complaints, and federal action against a company. John Hancock currently holds an above-average B rating.

Moody’s

Similar to A.M. Best, Moody’s long-term obligation ratings measure an insurer’s credit risk. John Hancock holds an upper-mid-grade rating of A1, representing a low credit risk.

Standard & Poor (S&P)

S&P ratings also measure an insurer’s credit risk. John Hancock earned a very strong AA- rating, the fourth-highest of 21 overall scores.

NAIC Complaint Index

The National Association of Insurance Commissioners’ Complaint Index compares the number of complaints registered against an insurer each year with that of other companies. The NAIC sets the average index score at 1.00. John Hancock has a current score of 0.33, significantly lower than the industry standard.

J.D. Power

J.D. Power’s annual U.S. Life Insurance Study measures overall customer satisfaction in four areas: annual statement and billing, customer interaction, policy offerings, and price. John Hancock scored 2/5 in the 2018 study.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Company History

The John Hancock Mutual Life Insurance Company was founded on April 21, 1862, in Boston, Massachusetts. Its founders chose one of our nation’s most prominent forefathers as their namesake to show their commitment to integrity and service.

What was originally established as a four-person company operating out of a single, small room has since grown to become the country’s sixth-largest provider of individual life insurance policies.

The company has since “demutualized,” becoming publicly traded in 2000. In 2004, it was acquired by Canadian-based financial services group Manulife Financial.

Now a full-service financial services company, John Hancock sells life insurance through three subsidiaries:

- John Hancock Life Insurance Company

- John Hancock Life Insurance Company of New York

- John Hancock Life & Health Insurance Company

John Hancock’s Market Share

In 2018, John Hancock held a 3.6 percent market share of all individual life insurance business in the country, representing $4,651,894,000 in direct written premiums.

The company doesn’t currently sell group life insurance policies, but still maintains a 0.02 percent market share based on $5,541,041 in previously written premiums.

As previously mentioned, the insurance arm of John Hancock Financial sells life insurance through three subsidiaries:

- John Hancock Life Insurance Company

- John Hancock Life Insurance Company of New York

- John Hancock Life & Health Insurance Company

As the name implies, the John Hancock Life Insurance Company of New York sells policies exclusively to customers in New York, along with John Hancock Life & Health Insurance Company.

The John Hancock Life Insurance Company is licensed to sell policies in the remaining 49 states, Washington D.C., and Puerto Rico.

From 2015-2018, John Hancock rose one spot from the seventh- to the sixth-largest writer of individual life insurance policies, though their market share has decreased.

John Hancock’s individual life insurance business has been holding fairly steady for the past four years.

They dropped slightly in market share from 3.7 to 3.6 but increased in ranking due to having written around $58 million more in premiums than closest competitor State Farm.

There is a razor-thin margin of only a few million dollars separating the insurers in the sixth, seventh (State Farm), and eighth (Transamerica) positions, with each holding a 3.6 percent market share.

John Hancock’s Position for the Future

John Hancock has experienced a slight but steady decline in market share over the past four years. Their share fell from 3.9 market share in 2015 to 3.6 in 2018.

During that time, they had a drop in direct written premiums from $4,749,494,000 in 2015 to $4,561,320,000 in 2016. They started to rebound in 2017, and have since increased to $4,651,894,000.

John Hancock’s fluctuation in market share could be because the company is in a bit of a transition period.

In 2016, the company stopped selling long-term care insurance, of which they were the second-largest carrier. During that time, they’ve also shifted to new, interactive life insurance policies.

Despite all of this change, the company is still in a good position for the future.

Along with their name, history, and financial strength, they are also backed by global giant Manulife, which currently services millions of customers in 22 countries and territories worldwide.

John Hancock is in a tight race for market share with seventh-place State Farm and eighth-place Transamerica. Both are right on Hancock’s heels, separated by the smallest margins.

State Farm has been steadily increasing its market share from 3.5 market share and $4,189,927,000 in premiums in 2015 to 3.6 market share and $4,593,999 today.

Transamerica is right behind them with $4,567,999,000 in written premiums.

John Hancock may trade market share positions with State Farm and Transamerica for the next few years, but there is no reason to think they won’t remain a top-10 insurer for the foreseeable future.

John Hancock’s Online Presence

John Hancock offers the ability to pay bills, file a life insurance claim, request a quote, and apply for specific term policies through its website.

You can request a quote and apply for certain term policies online, but for all others, you must call or email customer service, who will then refer you to an independent agent in your area.

John Hancock’s Commercials

Nearly all of John Hancock’s life insurance advertising over the past year has been for its guaranteed acceptance final expense insurance. These no-exam policies have smaller face values and are meant to cover funeral costs.

But that’s not all you probably know John Hancock for.

John Hancock in the Community

John Hancock is committed to giving back to the communities in which it operates, and does so through several key initiatives.

Corporate Giving:

John Hancock regularly awards grants to local non-profit organizations in two areas:

- Financial Empowerment

- Health and Wellness

Applications are available on their website.

MLK Scholars Program:

John Hancock believes that career readiness is the key to financial empowerment and security. To that end, the company recently pledged $1 million in grants to 65 non-profit organizations through its MLK Scholars program.

Each year, the program provides summer jobs to over 600 teens. It is the largest summer jobs program of its kind in the country.

The John Hancock Boston Marathon Non-Profit Program:

Since 1986, John Hancock has been the principal sponsor of the annual Boston Marathon. That year, they provided the first-ever prize money and have awarded more than $20.5 million to top finishers since.

As part of that sponsorship, John Hancock donates over a thousand runner entries through their Boston Marathon Non-Profit Program. Runners pledge to raise money for select non-profit organizations in exchange for their entry.

In 2019, the Boston Marathon raised $38.7 million, supporting 297 different non-profit organizations. John Hancock–sponsored runners alone raised $14 million of that total.

Their employees seem to like working for them, too.

John Hancock’s Employees

John Hancock currently employs nearly 8,000 people nationwide.

Overall, Glassdoor employee reviews for John Hancock average 3.5 out of five stars based on 507 reviews. In addition, 71 percent of current employees say they would recommend the job to a friend.

John Hancock consistently ranks among Forbes America’s Best Employers and Forbes America’s Best Employers by State (Massachusetts).

They have also been named one of Best Places to Work for LGBT Equality, earning a perfect score of 100 percent on the Human Rights Campaign Corporate Equality Index.

Shopping for Life Insurance

If you’re reading this review, you’ve probably already concluded that you need life insurance. If so, here are a few statistics to help validate your decision.

According to the 2018 Insurance Barometer Study from Life Happens and LIMRA:

- 35 percent of households would be financially impacted within one month of the primary wage earner’s death

- 90 percent agree that the primary wage earner should carry insurance

- 60 percent of all people living in the United States have life insurance

- 20 percent of those with a policy feel their coverage is insufficient

If you’re one of those without a policy or one whose policy might be insufficient, there are some things to keep in mind as you shop for a new policy.

In general, life insurance needs to cover two types of obligations: immediate and future.

Immediate obligations are the things that need to be paid soon after your death. These include funeral costs, medical bills, mortgage balances, and any other outstanding debt.

Future obligations are all of the expenses (planned or unexpected) that arise years after your death, such as college tuition for a child, retirement for a spouse, or medical emergency for a loved one.

If your family is dependent on your income, that future obligation also needs to include how many years’ worth of your annual salary you want to leave your family so they can maintain their current quality of life.

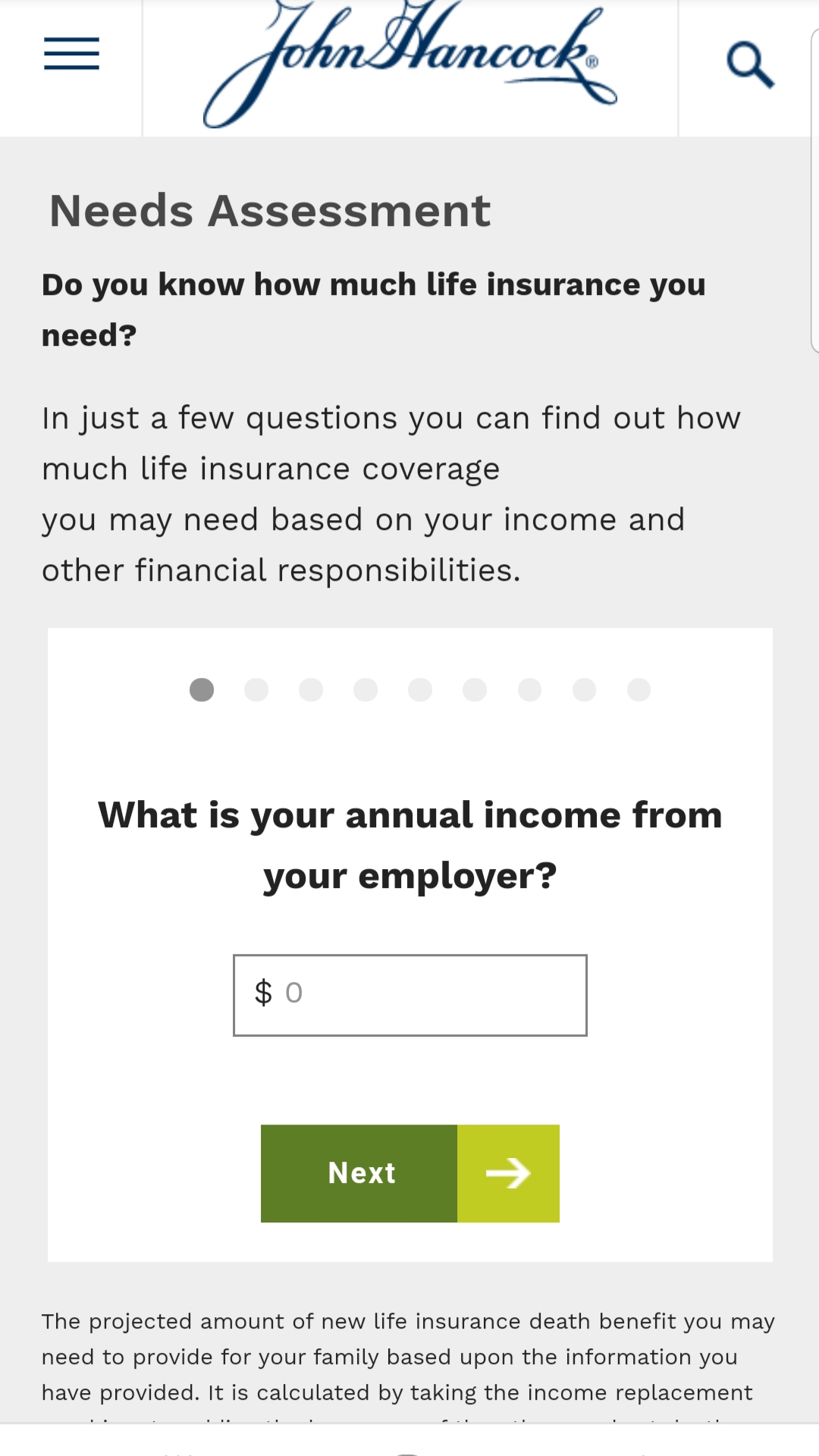

A life insurance agent or financial planner can help you determine exactly how much coverage you’ll need to cover all of those obligations. For now, here is an example using John Hancock’s life insurance calculator.

A wife and mother of two is the majority wage earner for her family, with an annual salary of $80,000. She has a remaining mortgage balance of $75,000.

The mortgage is the largest annual expense. Once it is paid off, the husband (who works) will need less overall income. Therefore, she plans to leave only five years’ worth of her salary.

She’d also like to establish a college fund of $25,000 each for both children. After factoring in an average funeral cost of around $7,500, your insurance needs are as follows:

- Immediate: $75,000 mortgage + $7,500 funeral costs = $82,500

- Long-term: $400,000 income replacement + $50,000 college tuition = $507,468

- Total: $532,500

That total means you would need a life insurance policy with a face value of around $550,000.

Average John Hancock Male vs. Female Life Insurance Rates

The following table illustrates how John Hancock’s average rates for males and females in key demographics compare to the average of the top 10 insurers by market share.

Life: Average-John-Hancock-Male-vs.-Female-Life-Insurance-Rates

| Demographic | Annual Premium: Male | Versus Average Top 10 Insurers | Annual Premium: Female | Versus Average Top 10 Insurers |

|---|---|---|---|---|

| 25-Year-Old Non-Smoker | $178.30 | -$0.24 | $172.50 | +$11.93 |

| 25-Year-Old Smoker | $440.20 | +$118.44 | $326.30 | +$77.55 |

| 35-Year-Old Non-Smoker | $189.80 | +$4.76 | $178.30 | +$12.39 |

| 35-Year-Old Smoker | $461.90 | +$101.67 | $353.40 | +$67.22 |

| 45-Year-Old Non-Smoker | $292.10 | +$24.21 | $241.50 | +$1.25 |

| 45-Year-Old Smoker | $777.10 | +$139.59 | $523.10 | +$29.90 |

| 55-Year-Old Non-Smoker | $533.60 | +$8.65 | $407.10 | +$0.16 |

| 55-Year-Old Smoker | $1,536.90 | +$172.81 | $949.00 | -$42.63 |

| 65-Year-Old Non-Smoker | $1,380.00 | +$106.88 | $937.30 | +$56.64 |

| 65-Year-Old Smoker | $4,091.90 | +$846.85 | $2,184.50 | +$50.81 |

| Average Non-Smoker | $514.76 | +$28.85 | $387.34 | +$16.47 |

| Average Smoker | $1,461.60 | +$275.87 | $867.26 | +$16.25 |

Coverage Offered

John Hancock offers several term, universal, and variable universal life insurance policies to meet your financial needs. You can also choose from multiple riders to further tailor your policy.

Types of Coverage Offered

Life insurance policies fall into one of two general categories, term or whole. Term policies only pay if the death occurs within a set time frame, usually between 10 and 30 years.

Whole life insurance policies have no term and pay whenever a death occurs, regardless of age. They have multiple variations: traditional whole life, universal life, and variable universal life.

John Hancock currently offers term, universal, and variable universal policies.

Term

A term life insurance policy is payable only if the death of the insured occurs within a specified period or before a specified age.

Once the term has passed, the insurer cancels the coverage. There are generally no refunds on the premiums paid. Some policies can also be converted to a whole policy before it expires.

The specifics of John Hancock term policies are as follows:

- Term: 10, 15, or 20 years

- Convertibility: Convertible during the first 10 years of the policy, or until age 70 (whichever comes first)

- Minimum: $100,000

- Maximum: None (Subject to individual consideration and underwriting limits)

- Issue Age: 18-80

Universal

Universal life insurance policies are adjustable and offer the flexibility to set monthly premiums and change coverage amounts.

Insurers typically charge higher premiums in the earlier years of the plan. The additional premium is then invested at a fixed interest rate so that it can grow to cover the eventual payout.

That savings element means the policy has the potential to grow a tax-deferred cash value beyond the face value of the policy, payable to the policyholder.

Universal policies also allow for loans or withdrawals from the cash value. The specifics of John Hancock universal policies are as follows:

- Flexibility: Face amount increases are not permitted; decreases permitted after the first year

- Interest: Guaranteed 2 percent interest

- Minimum: $50,000

- Maximum: None (Subject to individual consideration and underwriting limits)

- Issue Age: 0-90

– Variable Universal

Rather than being placed in an interest-bearing account with a fixed rate, variable universal policies allow you to invest your cash value in stocks, bonds, and money market mutual funds.

These policies come with the greatest risk, but also the most growth potential. The specifics of John Hancock variable universal policies are as follows:

- Flexibility: Face amount increases are not permitted; decreases permitted after the first year

- 20-Year No-Lapse Guarantee: Guarantees the policy coverage will not lapse during the first 20 years of the policy even if the net cash surrender value falls to zero, as long as premiums are paid

- Interest: Guaranteed 2 percent interest

- Minimum: $50,000

- Maximum: None (Subject to individual consideration and underwriting limits)

- Issue Age: 0-90

Burial & Final Expense

Final Expense policies (often called “burial insurance”) are special whole life policies with low face values meant only to cover funeral expenses and perhaps some small financial obligations such as credit card debt.

John Hancock offers a guaranteed, no-exam final expense policy with face values from $2,000-$20,000. Your payments never go up, and your coverage never goes down as long as you live.

Riders

Riders can be added to each policy to customize your coverage further. John Hancock offers the following:

- Total Disability Waiver Rider: If you become completely disabled, your premiums will be waived for the duration of your covered disability or for the duration of your policy

- Accelerated Benefit Rider: Allows you to access a portion of the death benefit if you become terminally ill

- Unemployment Protection Rider: If you become unemployed, your premiums will be waived up to an annual premium amount of $10,000

Factors That Affect Your Rate

Anything that increases your chances of dying early increases the chances the insurer will have to pay out on your policy. That risk is passed to you in the form of higher premiums.

Let’s take a look at some of the most common factors that affect your rate.

Demographic

Several demographics can have a big impact on your life insurance premium.

Age is one of the most important factors in determining insurability. Statistically, the more time has passed, the closer you are to death.

The older you are when you apply for a policy, the higher your rate will be. It can also limit the face value of your policy. The older you are, the less coverage you’ll be allowed.

Gender also plays a key role. Statistically, women live longer than men. For that reason, women typically enjoy lower life insurance premiums than men.

Marital status doesn’t directly influence your premium, but it could indirectly increase it. A marriage most often comes with shared finances and responsibilities. A married individual typically has more future obligations (spousal support, children’s tuition, etc.) than a single individual.

Higher coverage equals higher premiums.

Current Health & Family Medical History

The healthier you are, the longer you’re likely to live, which translates to lower premiums. To determine your overall health, insurers will require you to fill out a health questionnaire and may request access to your medical record.

Some may require a complete medical exam and bloodwork. Because many diseases have a hereditary component, many insurers will also examine the health history of your immediate family.

Even if a policy does not require a medical exam, underwriters have access to public prescription and Medical Information Bureau (MIB) records.

It’s important to be as honest as possible on the self-assessment.

High-Risk Occupations

By nature, some jobs are more dangerous than others.

For example, the Bureau of Labor Statistics’ Census of Fatal Occupational Injuries shows that police officers, firefighters, construction workers, and the like have a higher risk of dying on the job than — say — an insurance adjuster.

The more dangerous the occupation, the more likely an insurer is to pay out a death benefit, which means higher premiums.

High-Risk Habits

By that same token, high-risk habits outside of your occupation can also result in costlier life insurance.

The most common high-risk habit that insurers look for is tobacco use. Smokers almost universally pay higher rates than their non-smoking counterparts in every demographic.

For example, at John Hancock, a 35-year-old male non-smoker pays around $150 per year for a 10-year, $250,000 policy. A 35-year-old smoker pays $476 for the same policy. That’s an extra $3,260 paid over the life of the plan.

In addition to smoking, insurers will also ask about any other high-risk hobbies, such as mountain climbing, flying, or any other regular activity that has a high potential for injury.

Frequency is key here. A single experience isn’t going to result in a higher premium, but a regular, repeating high-risk hobby will.

Veteran or Active Military Status

Military status falls under the category of high-risk occupations. Most insurers charge higher rates to active duty military service members, and some don’t sell them policies at all.

Getting the Best Rate with John Hancock

Some simple lifestyle changes and some expediency can help you get lower premiums on your life insurance policy.

Insurers base their premiums on three factors: mortality, interest, and company expenses. They use statistical mortality tables to estimate how many people in specific demographics are going to die each year. Their rates rise or fall based on how many people in that demographic they insure.

They also adjust premiums based on current interest rates.

Insurers increase their profits by investing the premiums you pay in bonds, stocks, etc. If they expect a lower rate of return on those investments, they may raise premiums to make up the difference.

Insurers factor in their overhead expenses. The more they spend maintaining their daily operations, the more costs they’ll pass on to you. Rates can also vary from state-to-state, though the NAIC is currently encouraging states to adopt laws that would provide more uniformity nationwide.

With all of those variables, what can you do to get the best rates? Some things like gender, family medical history, and occupational risk are beyond your control. The best thing to do is to change what you can.

Be healthy. Eat better. Exercise. Monitor your blood pressure. Control your cholesterol. Anything you can do today to live a longer, healthier life will save you in the long run.

Stop smoking. If you smoke, stop, and stop soon. Many insurers require you to be tobacco-free for an extended period before giving you a non-smoking rate. John Hancock is unique in that they offer an immediate incentive to those who wish to give up tobacco.

Their Quit Smoking Incentive allows standard and preferred smokers to receive the standard non-smoking rate for the first three years of their policy, with the idea being that they will use that time to quit.

To maintain the non-smoking rate after year three, they must provide sufficient evidence that they’ve been tobacco-free for 12 consecutive months and submit to micro urinalysis.

Buy now. You can’t control your age, but you can choose how long to wait before buying a policy. Statistically, the older you are, the more likely you are to die during your term or before your universal policy matures to its guaranteed benefit. Therefore, the older you are, the higher the rate.

For example, at John Hancock, a 10-year, $250,000 policy for a 35-year-old male non-smoker costs around $475 per year. That same policy for a 45-year-old costs $985. That 10-year wait costs an extra $5,100 over the life of the policy.

Pay your premiums. It’s important to pay on time. Like any bill, late or non-payments on term policies result in penalties and could lead the insurer to cancel your policy.

Vitality discount. John Hancock launched their Vitality program in 2015, and have since incorporated it into all of their policies.

Vitality is a behavior change platform that makes each insurance policy “interactive.” The company rewards customers for everyday steps they take to live longer and healthier lives. Policyholders have two options: Vitality GO and Vitality PLUS.

Vitality GO: Vitality GO is offered on all life insurance policies at no cost. Policyholders have access to multiple fitness and nutritional resources, which they use to set personalized health goals.

Members track their progress through a simple app and on the Vitality website. As they reach key milestones, they’re rewarded with discounts at major brand outlets.

Vitality PLUS: For $2.00 a month, policyholders enjoy all the benefits of Vitality GO, along with the potential to save up to 15 percent on their annual life insurance premiums.

Members earn points and advance toward specific milestones by exercising, eating healthy, and getting regular checkups. As they achieve higher levels of fitness, their premium discount grows.

Users record their healthy activities using the app in conjunction with either a complimentary Fitbit or a discounted Apple Watch (for as little as $25).

As of January 2019, members who reach platinum status for three consecutive program years will also receive a one-year Amazon Prime membership.

https://youtu.be/XswX1TSQwfQ

Nearly all of John Hancock’s rates are higher than the average. Of those rates, the average rates for senior females, ages 55 and over, are least above average.

The only below-average rates are for senior female smokers. The rates for 55-year-old female smokers are about $43 below average, and 65-year-olds are $50 below.

John Hancock is also one of the few insurers to underwrite individuals who are HIV positive. They offer term policies with face values of $250,000 to $2,000,000 for those aged 30 – 65.

Coverage is subject to a strict adherence and favorable response to antiretroviral therapy (ART), and regular lab work showing the absence of significant immunosuppression. Applicants must also be free of other comorbid conditions such as hepatitis C or diabetes.

The premiums for universal life policies are dependent on many variables. As a result, John Hancock requires you to talk to an agent to receive a quote.

To give you an idea of how much a term life policy might cost, we’ve compiled a list of sample rates for a 10-year term for non-smokers at key ages.

Life: John-Hancock-Sample-Rates

| Age | $100,000: Male | $100,000: Female | $250,000: Male | $250,000: Female | $500,000: Male | $500,000: Female |

|---|---|---|---|---|---|---|

| 25 | $9.64 | $8.78 | $12.04 | $10.34 | $17.86 | $13.91 |

| 30 | $9.64 | $8.78 | $12.21 | $10.56 | $18.06 | $14.46 |

| 35 | $9.64 | $8.78 | $12.44 | $11.31 | $18.76 | $16.46 |

| 40 | $10.63 | $9.45 | $14.16 | $13.94 | $20.01 | $19.46 |

| 45 | $13.10 | $11.54 | $18.16 | $17.46 | $26.86 | $23.21 |

| 50 | $15.81 | $14.80 | $23.46 | $19.76 | $39.11 | $32.56 |

| 55 | $22.44 | $19.58 | $36.06 | $27.89 | $64.81 | $48.46 |

| 60 | $35.15 | $27.30 | $55.49 | $39.99 | $103.56 | $70.96 |

| 65 | $55.74 | $37.74 | $98.09 | $66.21 | $185.01 | $114.86 |

John Hancock’s Programs

John Hancock’s website includes several valuable tools and resources that can help you decide how much and what type of life insurance you need.

John Hancock’s learning center consists of an extensive blog that covers a range of topics in three main categories:

- Financial Fitness

- Health and Wellness

- Life Stories

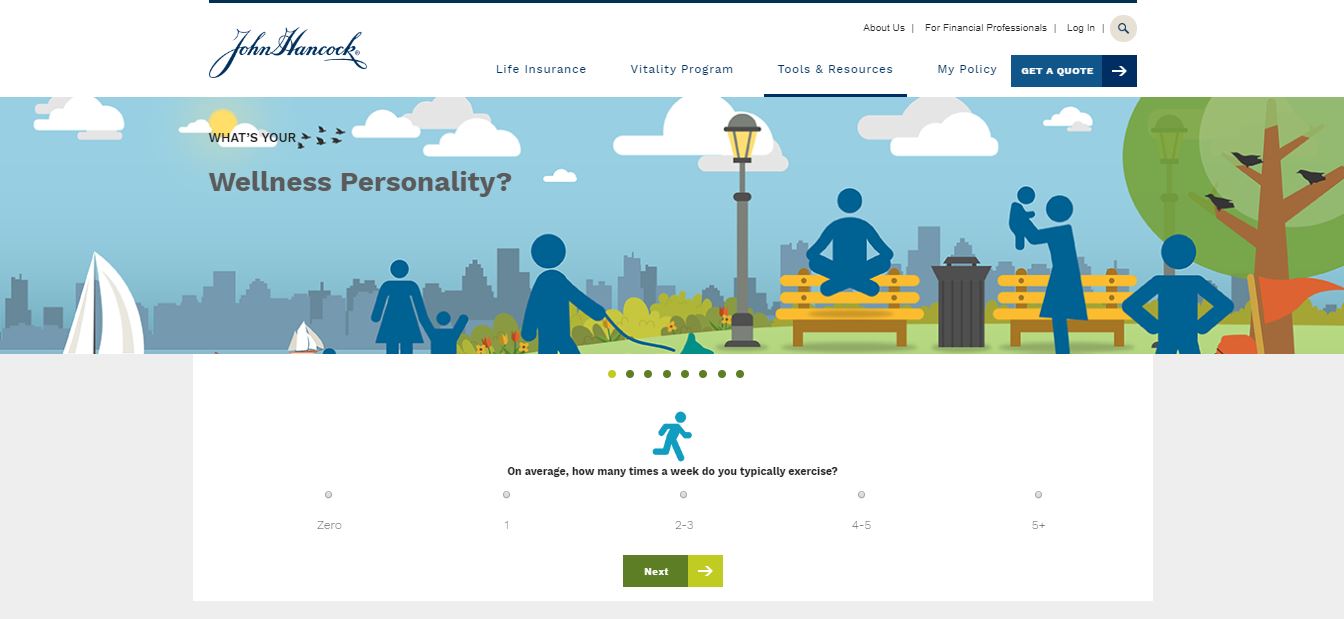

John Hancock also offers three interactive calculators and a wellness quiz to help you determine how much life insurance you need and what you can do to improve your overall health.

Life Insurance Calculator

Life Expectancy Calculator

Vitality Age Calculator

Wellness Quiz

Free Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Canceling Your Policy

If you need to cancel your life insurance policy for any reason, here’s what you need to know.

John Hancock doesn’t list any cancellation fees for their term policies, but there are generally fees for canceling any policy early in the term. Universal policies typically come with surrender fees, which is a charge deducted from the cash value of a plan when you cancel.

For a term policy, you will only receive a refund on any premiums you prepaid for an upcoming period. For a universal policy, John Hancock refunds any prepaid premiums as well as the surrender value of your policy, which is the cash value of your policy minus any surrender fees.

How to Cancel

The only way to cancel a John Hancock life insurance policy is to submit a physical copy of a Policy Surrender Form by mail.

You are free to cancel any policy at any time, though early termination of some term plans could result in penalties.

How to Make a Claim

The overall process of filing a death benefits claim with John Hancock follows general industry-standard steps:

- Initiate a claim

- Fill out company-specific paperwork

- Submit the paperwork along with a death certificate and any other requested documents

- Choose a disbursement method

- Receive the benefits

The specific process is as follows.

Filing a claim with John Hancock is fairly simple, with multiple ways to initiate the process.

You can start a claim online, over the phone, or with your sales agent.

- Online: The online claim center includes a simple form which asks for both the requester’s and insured’s personal information

- Phone: 1-800-732-5543

- Agent: Contact your local sales agent

After calling or filling out the online form, John Hancock will send you a claim package which includes a complete claim form as well as a checklist of all documentation required to process.

Once you fill out the form and gather all required documents, you can mail the package to John Hancock Life Insurance, Suite 1101, 1 John Hancock Way, Boston, Massachusetts 02217.

An examiner will begin reviewing your claim immediately, and the company will process your benefit payment within 10 business days.

You will then need to choose one of the following payment options: installments with interest, lump sum, or an interest-bearing account with check writing privileges.

You will need to complete a claim form and submit one certified death certificate along with the original policy (if you have it).

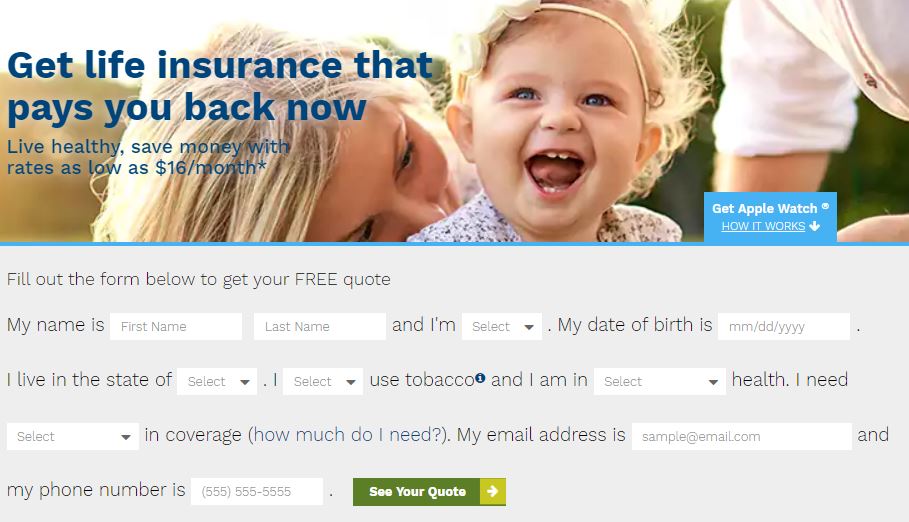

How to Get a Quote Online

It’s simple to get an online quote for a term policy from John Hancock. All you’ll need to do is head to the quote tool and enter some basic information.

#1 – Go to the Online Quote Tool

From the homepage, select the link for the online quote tool.

It’s in the top right corner of the screen.

#2 – Enter Your Information

Enter your personal and contact information into the quote tool.

Then, hit “Select Your Quote.”

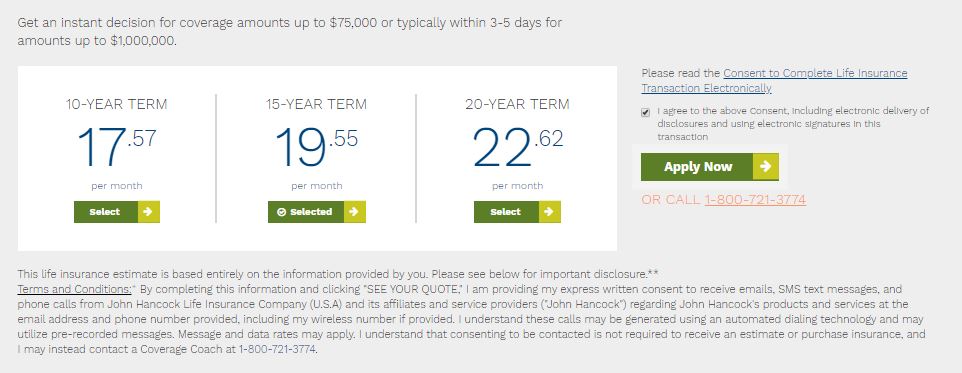

#3 – Get Your Quote & Apply

Once you submit your information, the tool will display quotes for a 10-, 15- or 20-year term policy.

You’ll then have the option to apply for a policy directly from the results screen.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Design of Website/App

The John Hancock insurance website is likely the first place you’ll go to buy and manage your policy. Here’s a preview of the overall web experience.

The John Hancock website is well designed and easily navigated, but you’ll have a hard time finding specific policy information if you’re shopping for a new life insurance plan.

Most of the policy information on the John Hancock website is a preview, meant to guide you to a local sales agent who will provide you with the specifics and help you determine your coverage needs.

If you have any questions about life insurance in general, a quick search through their blog should uncover the answers you seek.

The design of the website is a huge plus compared to the larger, cluttered, and harder to navigate John Hancock Financial.

The financial site contains much of the same life insurance information, but the insurance is much more streamlined and easier to use overall. The only drawback is that so much policy information you may be looking for is reserved for agents.

John Hancock doesn’t currently have a dedicated app for managing its life insurance policies. Fortunately, the site is optimized for mobile browsing.

You can easily access the same information from a computer on your phone or tablet.

Before you decide on John Hancock, consider the following pros and cons.

Pros & Cons

As with any company, there are pros and cons to shopping with John Hancock. Here are some of the biggest.

Pros

- A top-10 individual life insurance provider

- Financially sound

- Online quotes

- Online application for term policies

- No-exam term policies

- Wellness discounts

Cons

- Higher than average rates

- Most policy changes must be made using paper forms

- No long-term care coverage

The Bottom Line

While John Hancock is one of the oldest and largest life insurance providers, their higher-than-average rates could price them out of your consideration. There are plenty of companies with similar policies at lower rates.

Where John Hancock does stand out is in their low-cost, guaranteed acceptance final expense policies. If you’re just looking for enough insurance to cover your funeral costs, they’re worth a look.

They also earn points for their innovative Vitality program. If you’re committed to fitness and healthy living and can earn their highest annual discount, then their policies might be a perfect fit for you.

John Hancock FAQs

Here are some frequently asked questions about John Hancock and their policy offerings.

#1 – Does John Hancock offer a no-exam life insurance policy?

John Hancock doesn’t require a medical exam for their 10-, 15-, and 20-year term policies or their guaranteed acceptance final expense policy.

#2 – Does John Hancock offer any supplemental coverage?

In the past, John Hancock used to offer standalone and supplemental long-term care coverage, but they discontinued both products.

#3 – How do I make a payment on my John Hancock life insurance premiums?

You can have your payments automatically debited from your checking account every month by filling out an authorization form or make electronic payments from a savings or checking account online.

#4 – How easy is it to change my beneficiary?

You will need to fill out a beneficiary change form, which can be filled and submitted directly online or by mail.

#5 – Can I make withdrawals on my John Hancock life insurance policy?

Some of John Hancock’s universal life policies allow for a partial withdrawal or partial surrender on interest accrued during specific periods.

You can also take out loans against your cash value. Disbursements are made via mail after completing a dividend withdrawal form either online or by mail.

#6 – How long does it take for John Hancock to pay death benefits on a life insurance policy?

Death benefits are typically paid within 30 days of processing the completed claim packet.

#7 – Are the life insurance benefits taxable?

Life insurance benefits are non-taxable when they are paid directly to a beneficiary, such as a spouse or a child. However, if you name your estate as the beneficiary, the benefits become a part of the estate and are then subject to estate taxes.

#8 – Are all John Hancock life insurance policies available in all states?

Yes. John Hancock is licensed to sell all of its policies in every state through one of its three affiliates.

Start comparing life insurance rates now by entering your ZIP code in our FREE tool below!

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption